Providing financial resources and information on the microfinance industry to investors, borrowers, and professionals.

Microfinancing institutions (MFIs) were first created to help eradicate extreme poverty. Every year around 70% of India's citizens pay for healthcare out of pocket, forcing 39 million families into poverty. Using a low cost microloan to repair a leaky roof, purchase school clothes for their children, maintain a farm and keep food on the table, or pay off a hospital bill can give poverty-stricken communities a fighting chance. Microloans in the form of farm financing have proven doubly effective in that both increased income and food supply are provided as a result of the loan. Every year the Microcredit Summit Campaign hosts the world's microfinance participants to discuss the industry's challenges and opportunities. This campaign has reached over 175 million poor families globally.

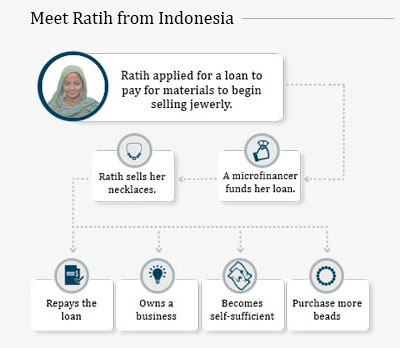

Low income communities commonly use microfinancing in the form of short term loans, to finance medical care, and to sustain small businesses that, in turn, provide borrowers income.

The future of MFIs relies on incorporating technology that eases access to microfinancial services. Digital platforms like cell phones can reach more qualified borrowers and cut up to 90% of the cost of the loan's transaction expense. Some cost reductions include allowing faster loan approval by more accurately assessing credit risk in a timely manner. With this technology, potential borrowers don't have to travel to a loan office or wait for paperwork to be approved. By digitizing microfinancial services, investors and borrowers can expect the microfinance industry to increase steadily into the next decade.

Even in the developed world, people sometimes need to borrow money and will take out short term loans in order to do so. The principle is very similar, but the amounts involved in microfinance are usually smaller (thusly the "micro" in the name of what is called "microfinance").